A credit score is a three-digit number that reflects your financial health. It ranges from 300 to 850 and shows how reliable you are at paying back borrowed money. A good credit score not only helps you get approved for loans but also ensures you get better interest rates and terms.

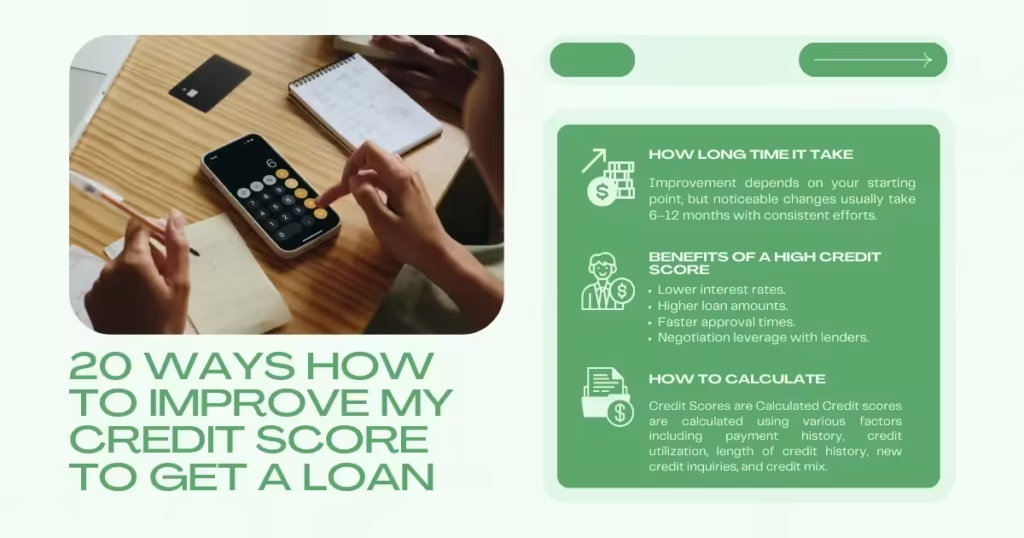

Credit Scores are Calculated Credit scores are calculated using various factors including payment history, credit utilization, length of credit history, new credit inquiries, and credit mix.

Table of Contents

Benefits of a High Credit Score for Loan Approval

A good credit score can lead to

- Lower interest rates.

- Higher loan amounts.

- Faster approval times.

- Negotiation leverage with lenders.

20 Ways to Improve Your Credit Score to Get a Loan

- Pay Your Bills on Time Making timely payments is crucial for a good credit score. Set up reminders or automatic payments to avoid missing due dates.

- Reduce Credit Card Balances Aim to keep your credit card balances below 30% of your credit limit. Paying down your balances can boost your score.

- Keep Old Credit Accounts Open The length of your credit history matters. Keep your older accounts open to show a longer credit history.

- Avoid New Credit Inquiries Each new credit inquiry can lower your score slightly. Apply for new credit only when necessary.

- Diversify Your Credit Mix Having a mix of different types of credit, like credit cards, loans, and mortgages, can improve your score.

- Regularly Check Your Credit Report Check your credit report at least once a year to spot errors and address them.

- Dispute Errors on Your Credit Report If you find any mistakes on your credit report, dispute them to get them corrected.

- Set Up Payment Reminders Use calendar reminders or apps to remind you of upcoming due dates.

- Use a Secured Credit Card If you have bad credit or no credit, a secured credit card can help you build or rebuild your credit.

- Become an Authorized User Ask a family member with good credit to add you as an authorized user on their credit card.

- Limit Your Credit Utilization Ratio Try to use less than 30% of your available credit. This shows lenders that you’re managing your credit well.

- Consolidate Your Debts Consider consolidating multiple debts into a single loan to make payments more manageable.

- Avoid Payday Loans Payday loans come with high-interest rates and can negatively impact your credit score.

- Negotiate Higher Credit Limits Ask your credit card issuer to increase your credit limit, which can lower your credit utilization ratio.

- Pay Off High-Interest Debts First Focus on paying off debts with the highest interest rates first to save money and reduce debt faster.

- Establish a Stable Employment History A stable job history can positively impact your credit score and loan applications.

- Use Credit Responsibly Only borrow what you can afford to repay and avoid maxing out your credit cards.

- Consider a Credit-Builder Loan These are small loans designed to help you build credit. Repaying them on time can boost your score.

- Make Multiple Payments Each Month Making smaller, more frequent payments can help keep your credit card balances low.

- Seek Professional Help if Needed Consider credit counseling or professional credit repair services if you’re struggling to improve your score on your own.

How Long Does It Take to Improve a Credit Score?

Improvement depends on your starting point, but noticeable changes usually take 6–12 months with consistent efforts.

Monitoring and Maintaining Your Credit Score

Using Credit Monitoring Tools These tools can help you track your score and alert you to any changes. Importance of Regular Credit Checks Regularly checking your credit report helps you stay on top of your financial health and spot any errors.

How a High Credit Score Affects Loan Approval

A high credit score makes you more attractive to lenders and increases your chances of loan approval. Better Interest Rates and Terms Higher scores often lead to lower interest rates and better loan terms, saving you money in the long run.

Common Myths About Credit Scores

Checking your own score doesn’t affect it. This is a soft inquiry and has no impact on your score. Closing Old Accounts Helps Closing old accounts can hurt your score by shortening your credit history. Only Credit Cards Affect Your Score Loans, mortgages, and other types of credit also impact your score.

Long-Term Credit Health

Building Good Financial Habits Stick to a budget, avoid unnecessary debt, and pay your bills on time. Importance of Emergency Savings Having savings can help you avoid relying on credit in emergencies and keep your financial health stable.

Conclusion

Improving your credit score takes time and effort, but it’s worth it. By following these tried and tested ways and maintaining good financial habits, you can boost your score and increase your chances of getting the loan you need with favorable terms.

FAQs

How long does it take to improve a credit score?

It can take a few months to a year to see significant improvements.

Can I get a loan with a bad credit score?

Yes, but it will come with higher interest rates and less favorable terms.

What is the fastest way to boost my credit score?

Paying off outstanding debts and making timely payments.

How often should I check my credit report?

At least once a year, or more frequently if you’re planning to apply for credit.

Do joint loan applications affect my credit score?

Yes, both applicants’ scores are considered, and the loan will appear on both credit reports.